The first rule of accountancy is that for every debit there must be a credit and if this rule is taken to its logical conclusion then for every Income and Expenditure report there must be a Balancing Statement.

And yet, in Service Charge Accounting there are many circumstances when accounts are prepared without a Balancing Statement. Examples of this include, accounts prepared under a section 21 demand, commercial service charge reconciliations and service charge accounts prepared where there is no requirement to hold service charge funds in clearly identified and separated client trust bank accounts.

To underestimate the importance of the Balancing Statement is a mistake as it provides valuable information to leaseholders about cashflow, liquidity and stewardship of the service charge funds.

TECH 03/11 – Best practice guidance

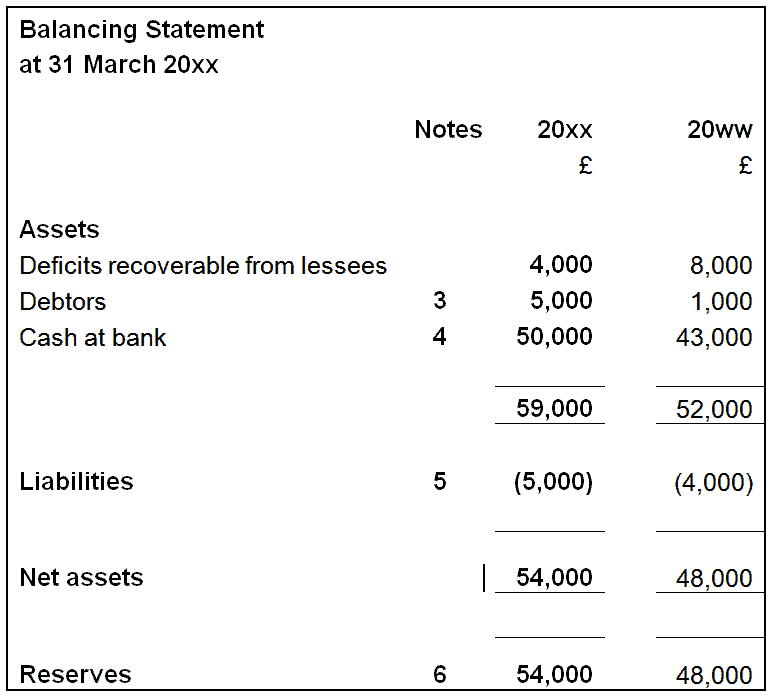

Appendix C to TECH03/11 gives an example of a Balancing Statement. The suggested layout is as follows.

What to look for in a Balancing Statement

Analysis of these balances can reveal important information to the reader of the accounts.

Deficits recoverable

This figure should be reconcilable to the deficit for the year on the Income and Expenditure report. If this is not the case then the balance may include deficits that go back over 12 months and therefore there is a possibility that these amounts may not be recoverable from lessees. This type of situation should be investigated by the lessee if the reasons are not immediately obvious or disclosed in the notes to the accounts.

Debtors

This figure includes the amounts owed by lessees at the year end. A significant increase in debtors from one year to the next may indicate a service charge dispute, weak credit control or an inability of lessees to meet their service charge demands. Lessees should always seek an explanation for a large increase in debtors from one year to the next.

Cash

A disclosure note should detail that the cash is being held in trust in designated bank accounts and in accordance with section 42 of the Landlord and Tenant Act 1987. This is one figure that every lessee needs to be aware of and the reasons for any significant movement in the balance over the year should be transparent from the accounts.

Liabilities

This includes all amounts that are owed by the service charge funds. It includes amounts for services provided and invoiced in the period that are still to be paid for at the year end. It also includes accruals or amounts that are charged to the service charge funds for invoices that have not been received at the year end. A good example of an accrual is an estimate for a utility cost relating to a past period. Lessees need to be aware of accruals and the makeup of the balance. Further explanation should be included in the notes to the accounts.

If there is a surplus for the year rather than a deficit then it will be included in Liabilities as it represents amounts owed by the service charge funds to lessees.

Reserves

All movements into and out of reserves should be disclosed either in the notes to the accounts or on the face of the Balancing Statement. Lessees should always ensure that that the reserve balance is more than the cash balance in Assets. If the reserve balance is less than cash then it indicates that the reserves are being used to fund the short term cash requirements of the property. This should be questioned as it indicates poor cashflow management.

Conclusion

The Balancing Statement contains so much valuable information to the leaseholder that it is difficult to understand why any set of service charge accounts would exclude the statement. It is a mistaken belief that the only information a leaseholder needs is an Income and Expenditure report for the year. A Balancing Statement together with accompanying notes are equally as important and the three components together give a much clearer picture of how service charge funds have been handled during the year.

In the modern world of professional property management no leaseholder should ever be subjected to the curse of the missing Balancing Statement.

Written by Haines Watts