You should see in the notes to a set of service charge accounts under ‘Accounting Basis’ something stating that the service charge accounts have been prepared in accordance with the provisions of the lease.

Below we have set out below some of the parts of the lease which link into service charge accounts.

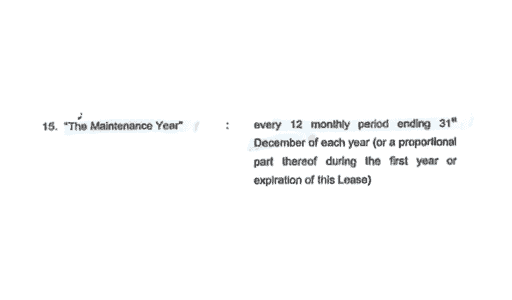

Service charge year end

Here is a typical extract from a lease:

This is setting out that service charge accounts should be drawn up to 31 December every year.

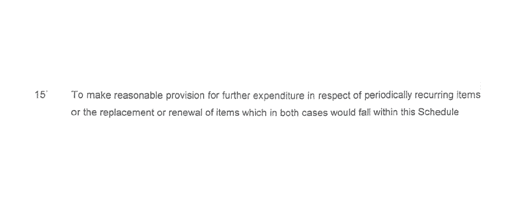

Expenditure permitted to be part of the service charge costs under the lease

There will be a section of the lease which sets out the allowable expenditure for the service charges. Typical clauses will include things such as:

- Repairs to the development

- Inspection of plant and equipment, repairs and replacements

- Internal redecoration – every 5 years

- External redecorations – every 3 years

- Cleaning and lighting in communal areas

- Gardening

- Car parking signs

- Refuse

- Maintain parking space

- Window cleaning

- Provide buildings insurance

- Public liability insurance

- Accountancy fees

- Management fees

The proportion of costs each lessee should pay

Somewhere in the lease there will sometimes be a specific percentage or fraction. e.g.

“1/9th of expenditure on services in respect of the development” or “20% of the service charge expenditure specified in Clause X”.

Fairly often the lease states something like “a fair and reasonable proportion of the expenditure on services in respect of the building”.

Reserve fund

If a reserve fund is been collected to save funds for future projects then there should be a clause in the lease permitting this.

Here is a typical extract:

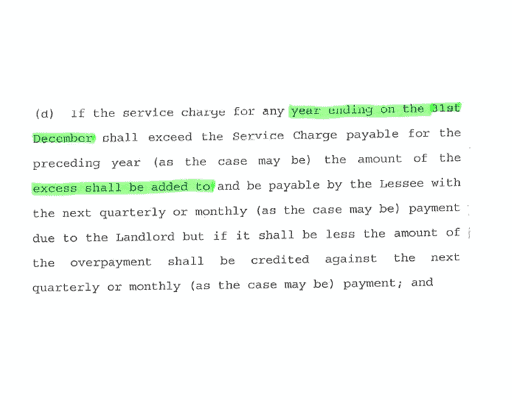

Treatment of surplus or deficit

If the service charge expenditure for the year has been larger than the service charge income invoiced then there will be a deficit. This deficit will be shown on the balance sheet of the service charge accounts as an asset of the service charge (money owed to the service charge).

If the service charge expenditure for the year has been smaller that then service charge income invoiced then there will be a surplus. The surplus will usually be shown on the balance sheet of the service charge accounts as a liability of the service charge (money owed by the service charge).

Almost without fail leases state that the deficit can be collected from the leaseholders and normally the lease states that the surplus should be collected from the leaseholders – such as in this clause:

Note however that sometimes the lease will state that the surplus should be transferred into the reserve fund.

The service charge accounts should be prepared by the property manager and certified by independent accountants with regard to what the lease says.